Tax Tip MythBuster: 7 Canadian Small-Business Tax Myths That Could Cost You Thousands

Every tax season, Canadian entrepreneurs scroll TikTok, Instagram, and YouTube and hear the same thing:

“Just write it off!”

“Buy a heavy truck and avoid taxes!”

“My accountant can deduct anything for you!”

This mythbuster clears up the most damaging misconceptions — and replaces them with CRA-compliant advice that actually reduces your tax bill.

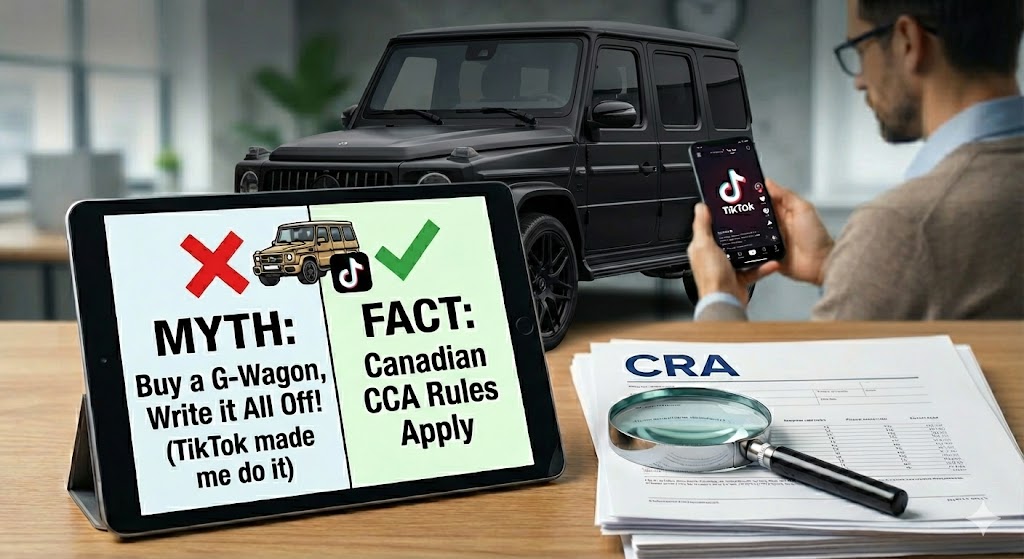

Myth #1: “If a U.S. content creator said it, it must apply in Canada.”

Absolutely not.

American creators talk about:

• Section 179 expensing

• Bonus depreciation

• 6,000-lb vehicle deductions

• 100% immediate SUV write-offs

None of these rules exist in Canada.

Canadian businesses follow Capital Cost Allowance (CCA) — a depreciation system with classes and rates, not instant write-offs.

Myth #2: “A truck over 6,000 lbs is a full write-off in Canada.”

This is a U.S. only rule.

Weight has zero impact on Canadian tax deductions.

How it actually works in Canada

Passenger Vehicles (CCA Class 10.1)

• Cost limit: $36,000 + tax

• 30% declining balance

• Business-use only

• Half-year rule applies

Motor Vehicles / Work Trucks (CCA Class 10)

• No $36,000 cap

• Still depreciated over time

• Still based on business use

No Canadian rule gives you an automatic full write-off because of vehicle weight.

Myth #3: “My accountant can write off anything.”

Let’s channel Biggie for a second:

“Phone bill about two G’s flat.

No need to worry, my accountant handles that.”

Iconic line. Terrible tax advice.

CRA requires every expense to be:

• Reasonable

• Directly related to earning business income

• Backed by documentation

Your accountant cannot turn personal expenses into business deductions — even if they’re paid from the business account.

Myth #4: “If I pay for it with my business account, it becomes a business expense.”

Wrong — and risky.

Personal spending from the corporation may create:

• A shareholder benefit

• Taxable income

• Shareholder loan issues

• CRA penalties

Business and personal spending must remain separate.

Myth #5: “If I use something sometimes for business, I can write off 100%.”

Mixed-use items must be allocated.

Home internet — deduct the business-use portion.

Cell phone — rarely 100% business.

Company vehicle — personal driving creates a taxable benefit.

Lack of mileage logs is one of CRA’s biggest audit triggers.

Myth #6: “Bank statements are enough for CRA.”

No — CRA requires proof of purpose.

Bank statements only show money leaving your account.

They do not prove:

• What was purchased

• Why it was purchased

• Whether it was business-related

• Vendor details

CRA can deny deductions without proper receipts, invoices, or logs.

Myth #7: “Write-offs reduce my taxes… so I should buy more stuff.”

A $10,000 write-off does not save you $10,000.

If your tax rate is 15%, it saves you $1,500 — but costs you $10,000 in cash.

Smart businesses invest in assets that:

• Generate revenue

• Improve efficiency

• Reduce future costs

Tax planning should support profitability, not justify unnecessary purchases.

The Truth: Tax Planning Is About Strategy — Not Shortcuts

There’s no U.S. loophole.

No viral TikTok hack.

No heavy-truck trick that replaces real tax planning.

Strong Canadian tax planning includes:

• Clean bookkeeping

• Proper mixed-use allocation

• Understanding CCA classes

• Good documentation

• Strategic asset purchases

• Year-round planning

Done right, it lowers taxes and protects you in a CRA review.

Need Real, CRA-Compliant Tax Strategy?

MiAccounting helps Canadian entrepreneurs stay compliant, stay organized, and stay profitable — without falling for tax myths.

Book a call today and get real strategy that actually works.